Hello Everybody,

Hope you all had a great October 🎃!

I know many of you celebrated Halloween 👻 last week and probably have homes full of candy🍬 ! If you’re like me, you’ve been on a steady diet of Mini Kit-Kats, Rocket candies, and of course Famous Amos cookies! (Or is that just me?!) lol 😆😅!

Anyway…I digress!…you may NEED a few candy bars after this update 📈📉😮!

And with that, here’s the update!

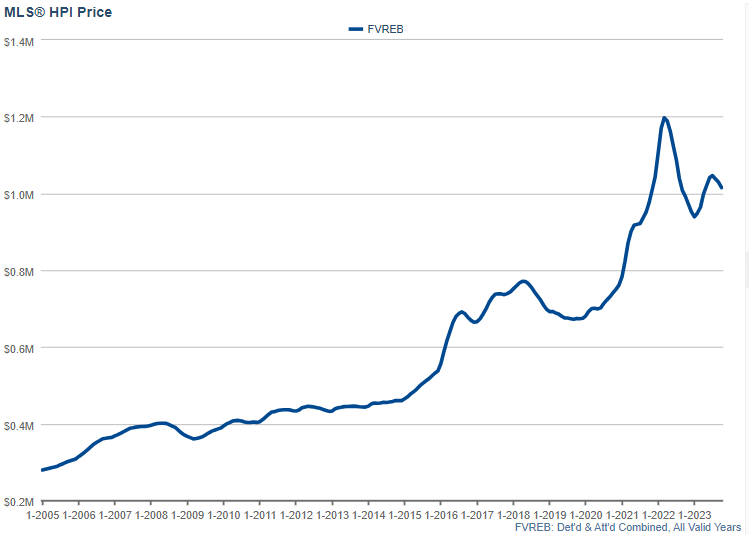

Home Prices

Overall in the Fraser Valley, October saw an even greater decline in the Combined Detached and Attached Housing Price Index (HPI) than it did in either of the last two months;

- October -1.4%,

- September -0.9%

- August -0.9%

As I’ve been stating since the end of July, prices have been falling just about everywhere since mid-July.

Another way to look at prices is that now prices are back down to where they were roughly in the following months (Rounded to the nearest month):

- April 2023 (while prices were increasing until July 2023)

- September 2022 (which also marked the second-slowest September in recorded history for sales volume)

- November 2021 (this is when prices were increasing by a single digit % per week in the frenzy of record-low interest rates!).

Now let’s move on for now and come back to prices later!

Sales Volume:

While October not only saw price fall nearly 1.4% since last month, it also had sales volume drop to near-record breaking lows for the month with only 918 posted sales (When looking at All Property Types). This marks the third lowest sales volume for the month of October ever recorded. (2022 was second lowest at 852 sales, and 2008 was the lowest at 695). Nearly every month from September of 2022 right up until now has been within the slowest 3 of its respective month.

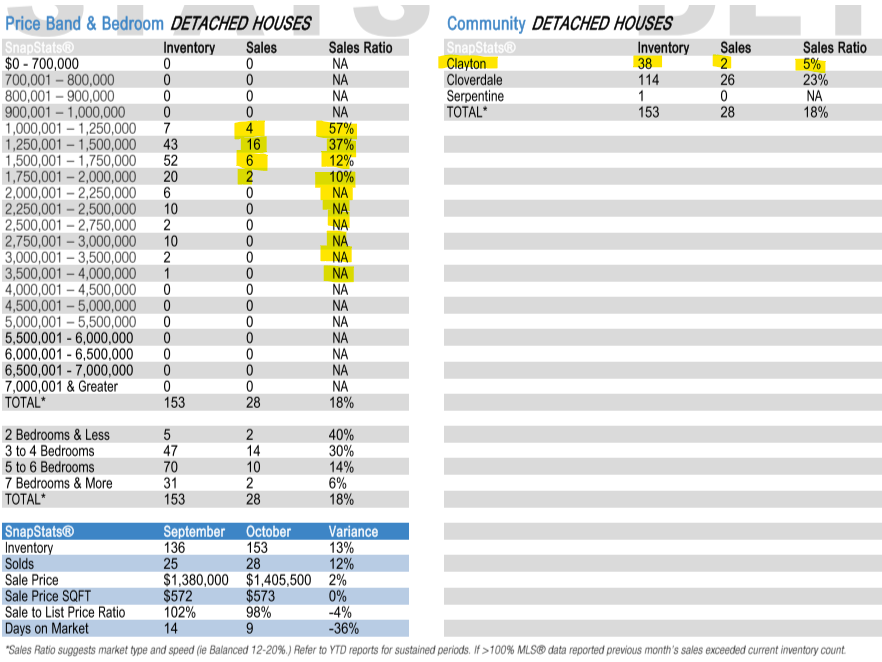

Now let’s jump into What is selling! We’ll use Two Areas for a deeper dive:

Cloverdale / Clayton

From this table what you can see is that while homes priced between$1,000,000 and $1,500,000 have been selling quite well with sales ratios of between 57% and 37%, homes above those values drop dramatically to12% in the $1,500,000 – $1,750,000 price category and 10% in the $1,750,000 – $2,000,000 price category. Once you go over that, the 31 homes listed above $2,000,000 didn’t have one sale Furthermore, when you look at the areas of Cloverdale on the right-hand side of the table you can see that while Cloverdale had a 23% Sales Ratio, Clayton Heights only had a 5% sales ratio which is the second lowest on record since 2008.

The answer here is likely two-fold:

1.) Homes in Clayton are more expensive and homes at this price simply aren’t selling in this market as you can see.

2.) Clayton has a disproportionate number of investors who own homes there because of the 3-dwellings-per-home style homes (Coach homes above the garage and a basement suite). The additional suite per home was seen as a big attraction to investors so the area became very heavily investor-owned. As interest rates have climbed to where they are today,most of these homes have negative cashflow every month of at least $2,000 to $3,000 per month so which has caused saturation in the market where in August there were only 3 homes on the market that had a coach home and today there are 16 and climbing.

Now let’s dig into Inventory…

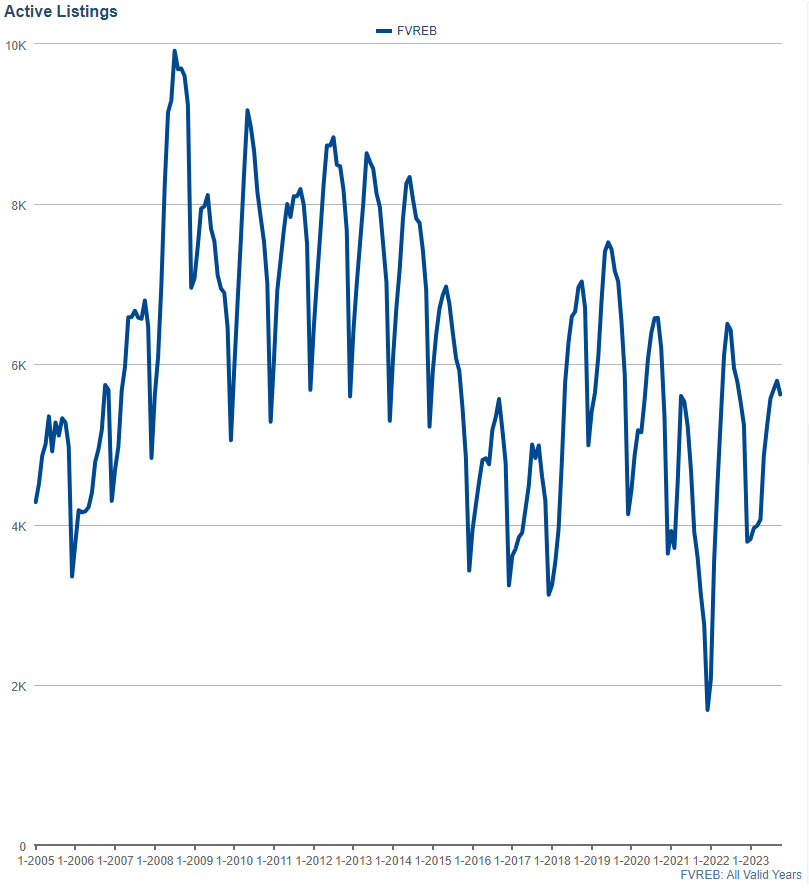

Listings

While both prices and sales volume decreased in October, one might expect the number of active listings to possibly increase based on the low sales volume, but instead, inventory also decreased, decreasing from 5,795 to 5,625 (a 3% decrease). This marks the seventh-lowest number of active listings ever recorded for October…but this is compared to the fourth-lowest number of active listings in September! This would seem to indicate inventory is perhaps increasing in relative terms! And let’s pause here for a second – why do I state this is bad news? Well here’s one reason, if prices are falling now with inventory coming from recent near-record lows…what will happen when inventory continues to increase, (as already evidenced)…Well if we go back to the regular laws of supply vs demand we would see that an increased supply, (isolated from other factors) would put negative pressure on the valuations and cause prices to come down (and in this case, accelerate the fire with even more fuel)!

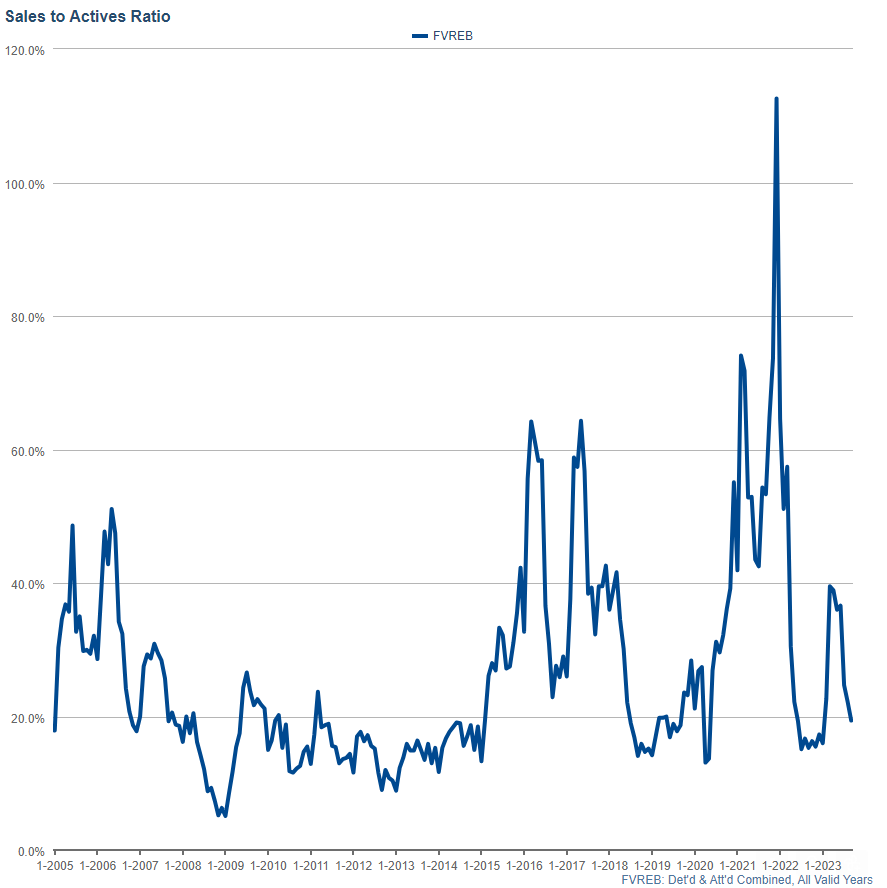

The below graph is also very telling because it represents the ratio between how many sales occur in a month vs how many active listings are on the market. The higher the ratio, the more of a seller’s market it is and the lower the ratio, the more of a buyer’s market it is. If there are 100 homes listed and 16 sell, for example, we’d say that there was a 16% sales to active ratio. Currently, for the month of October, we saw an overall sales ratio for the Fraser Valley of 16.4% (However in the luxury market this was closer to 5% and in the lower-end market, many areas say 40% or higher!)

My Forecasting:

Let’s keep this month’s update crisp and to the point. We can focus on 3 key indicators to understand the market’s direction—here they are:

1.) Mortgages Rates

With rates so high now for new mortgages, it’s important to consider just how many Canadians are paying these higher new rates and how many might be on lower fixed rates that haven’t renewed yet. According to the Bank of Canada as of July 2023, “About one-third of mortgage holders have already seen their rates increase, and the Bank of Canada forecasts that just about every borrower will experience the same in the next three years. (Daniel Munoz/Reuters)”. This stat is factoring in all mortgage types, both fixed and variable.

If prices are already falling and 2/3 of Canadians haven’t even felt the pain of these rates yet, one can only assume things could likely get worse. To what degree is hard to say but it doesn’t sound good. Many will say that interest rates will likely be lower (than today) in 2024 and into 2025, which is likely true, but still would likely be far higher than the record low levels of 2020.

2.) Rental Property Cash Flows

With interest rates as high as they are, and likely to remain higher, for longer,rental properties have become dramatically different to own. Someone who purchased a home at 3% interest rates, might have the rent cover all the expenses of the house referred to as “breaking even” OR may have potentially had some positive cash flow if the home had a secondary suite or the like. The difference is NOW, that same rental property (at 6% to 7% interest) may be negative cash flowing anywhere from $500 to $4,000 a MONTH! This is something that is becoming more and more untenable and this has and will continue to lead to more rental properties having to be sold due to not being able to afford that much per month.

In BC, nearly a quarter of all homes are owned by investors. 1/3 of all condos are investor-owned. This is more than any other province so this could have a major impact.

3.) Inflation

Canada’s Inflation Rate is back up to 3.8% as of September 2023, up from its recent low of 2.81% in June. Rent, groceries, and energy costs (not reflected in that inflation number, but factored in nonetheless) have skyrocketed across Canada, especially in our Fraser Valley and Vancouver areas. The Bank of Canada has a mandate to keep inflation between 1% and 3% and it is unlikely that they will start lowering the interest rates until they achieve that goal or something close to it. When we factor in how many months that might take to happen and then how long to proceed before the first decrease in rates – there is no way to be sure! I estimate rates start coming down a little bit sometime around mid-OKAY to the end of 2024. I’ve seen arguments for it being a bit sooner and some as long as the end of 2025 but there are too many factors to know exactly!

WHAT SHOULD YOU DO?

This question gets more complicated every month 🤣!

Essentially if you are a first-time home buyer, I would make sure you are fully pre-approved and working with your realtor now to get sent listings. Regardless if you aren’t going to buy right away. You’ll want to get your financing in order and explore that fully with your broker/banker/realtor to see what’s possible and then from there, you can have a much better idea of what to expect. Then you can see if it makes sense to purchase something now or whether you want to possibly wait. There are trade-offs when it comes to interest rates and speculating the market – always best to have more information than less 🙂

If you are upsizing then now may be one of the best times to consider making the move as you’ll “save” far more than you’ll “lose” peak to trough of the current market. The higher priced homes have come down farther than your lower priced home and the delta between those numbers has decreased for many making a move that was impossible before in the rising market, possible now.

If you are downsizing then I would be exploring options with your broker and realtor to see if there’s a way to accomplish your goals sooner rather than later or possibly even consider other options. Much of all of this would depend on the stage of life you’re in and if you’re retired and/or have a working income etc.

As always, I hope you found this helpful and please reach out any time with any questions or feedback!

Cheers!

Until next time,

– Corbin

Corbin Chivers

Personal Real Estate Corporation

REALTOR®

corbin@callcorbin.ca

www.facebook.com/callcorbin

www.callcorbin.ca